財務計算專題:期貨與選擇權

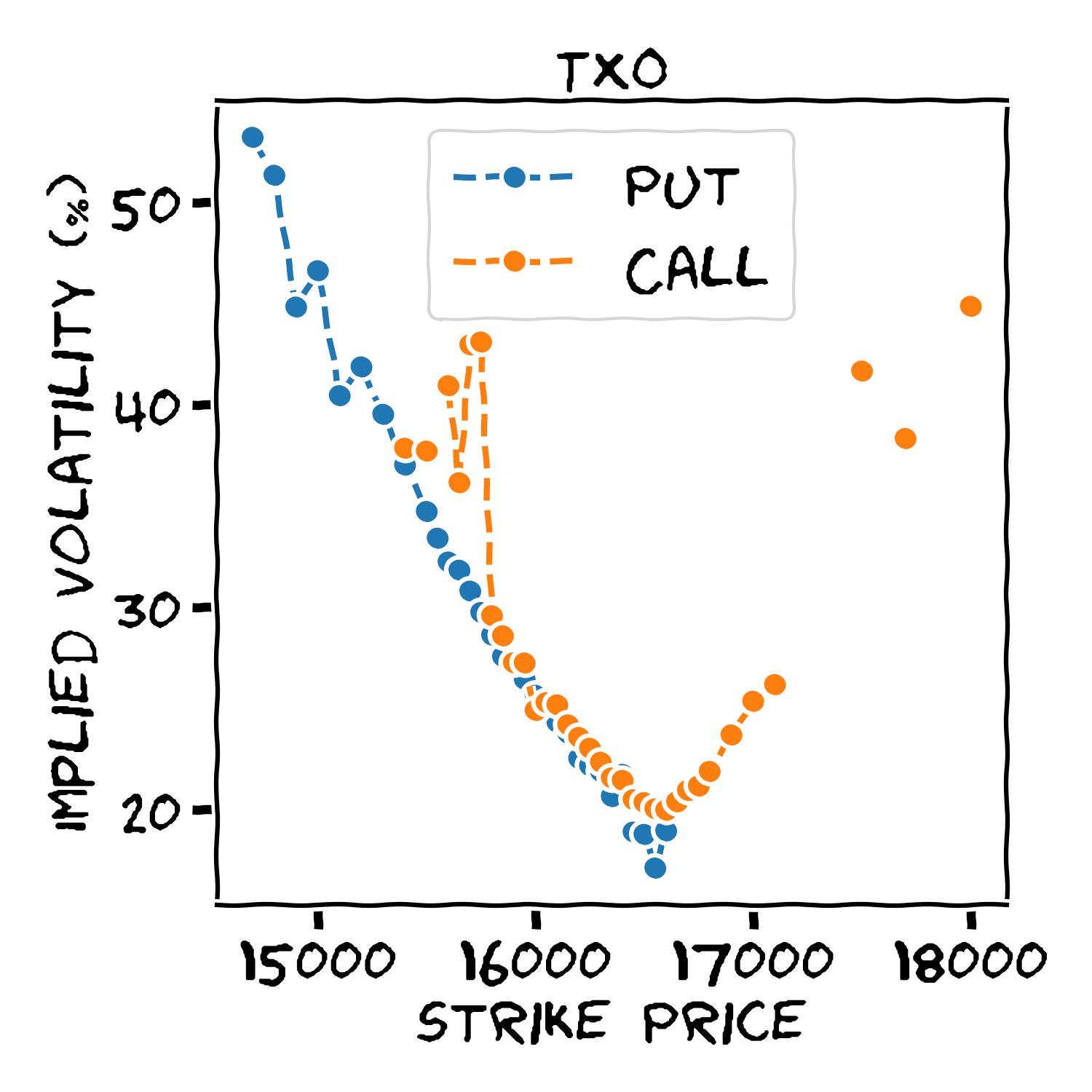

本課程將介紹期貨與選擇權的定義與功能,尤其我將深入解說選擇權的定價原理,並提供學員 Python 或 Excel 的範例程式修改,最後初步介紹各種選擇權的組合單。學員透過本課程可以了解期貨與選擇權的基本功能,並能夠自行計算選擇權的重要參數,諸如隱含波動率 (implied volatility) 與 delta 等,進而在操作期貨與選擇權時有客觀量化的數據利於調整投資組合。

歡迎對選擇權等衍生性金融商品有興趣的同學一同參與。

# 參考書目

[0] John C. Hull, Options, Futures, and Other Derivatives, 10/e, 2017

[1] Colin Bennett, Trading Volatility: Trading Volatility, Correlation, Term Structure and Skew, 2014

[2] Dan Passarelli, Trading Option Greeks: How Time, Volatility, and Other Pricing Factors Drive Profits, 2/e, 2012

[3] Alireza Javaheri, Inside Volatility Filtering: Secrets of the Skew, 2/e, 2015

[4] Dinabandhu Bag, Valuation and Volatility: Stakeholder's Perspective, 2022